Convertible Notes for Gaming Startups

When a startup is raising funding for the first time, the question is, what is the format that the money will come into your company?

There are two prevailing instruments. You have a convertible note and an equity-based funding round called the priced round. These are very different from each other.

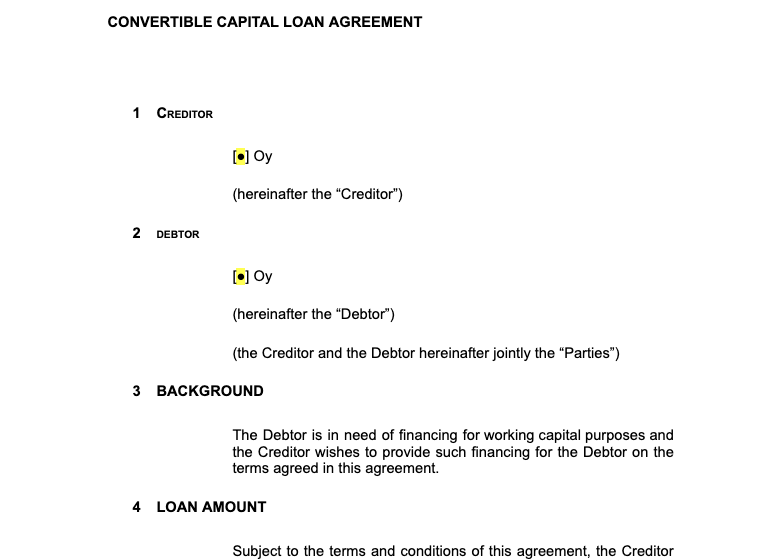

Convertible note

A convertible note is a loan from the investor to the company. But since we call it convertible, it means that it converts to equity at some point in the future, when an equity-based funding round or another event like an exit happens.

In this conversion event, the loan converts into percentages in the company, and new shares are created for the company’s investors.

Why is the convertible an attractive format of financing in the early stages? Here are a few reasons:

- No lengthy negotiations are needed; no new shareholders’ agreement is required because new shares won’t be created yet.

- Cheap: less legal help needed. It’s just one document.

- Flexible: Sign each investor individually as soon as they commit. Unlike the priced round, where all investors sign the same papers, startups could issue even dozens of notes over months as more interested investors show up.

The main answer is that the note is a “bridge” financing instrument, which awaits a priced round to happen at a later stage. When the priced round happens, the company goes and raises around, and then there’s a need to do all the proper paperwork, with a new shareholder’s agreement, a board of directors might be created, new share classes get created, etc.

Terms of a convertible note

Let’s cover the terms of the convertible note.

- Loan amount. This is the investment amount, which the investor will be wiring to the company’s account after the note has been signed.

- Valuation cap. This is the valuation maximum that the conversion won’t exceed. Let’s say the investor invested $20k at a $2m valuation cap. Once a priced round happens, the pre-money valuation is $4m. The investors in the priced round will get their money converted to shares at $4m pre, but the note investors will get them converted at $2m pre.

- Discount. If the priced round happens at a lower valuation than the valuation cap, a discount will be applied. If the investor invested $20k at a $2m valuation cap, with a 20% discount, and the company fails to raise a bigger round in the near future. Why would this happen? Because of a failed launch of their game, there can be many reasons. Anyways, the company ends up raising a $1m pre-money priced round, but the investors in the note will get them converted at $0.8m pre because they got the 20% discount.

- Maturity: This is also known as the due date when the note will automatically convert into shares. The valuation cap is often applied as the valuation cap for this conversion. The date is usually placed a few years into the future to progress towards a bigger priced round.

- Interest: A convertible note is a form of debt or loan. As such, it usually accumulates interest, usually between 4-8% between the point when you sign it and when it converts. This amount is usually converted as part of the overall amount in the next round. For example, if you have an annual interest rate of 8% and you have a note of $20k, then you’d convert $20.4k after a year.

Words of warning

When dealing with convertible notes, which haven’t been converted to equity, it’s hard to pinpoint the number of shares that the company has already committed to investors. Let’s say you have raised half a million ($500k) in several convertible notes, and you now want to raise three million ($3m) in a priced round. How do you calculate the percentage that is going to each investor?

There’s a great calculator that Carta has created. I suggest you check it out here: https://safes.carta.com/.

Example video

This is a clip from my online course, Pitch Your Games Company, where I walk you through all the details of fundraising for a games company. In this clip, I give an example of a $100k note-getting converted in the priced round.

What’s a SAFE?

The SAFE, which stands for “simple agreement for future equity,” is a

simplified version of the convertible note, created by the Bay Area-based startup accelerator YCombinator. It’s commonly used in the United States as it helps with some of the startup’s details.

The SAFE isn’t a loan instrument, and it doesn’t talk about maturity or interests, making it more startup-friendly as there’s no back date for a priced round to happen or that no interest needs to be calculated.

I don’t have experience applying SAFE documents outside of the United States, and I would stick to convertible notes based on the country-specific templates below.

Templates

I want to share convertible note templates for different countries. The reason for using templates for other countries is that the legality can vary per country, so it makes sense to use the template for the country where the company legally resides in.

Finland

Convertible note — to learn how to fill this out, here’s a video.

This note was created by Kimmo Reina from Bird & Bird (IMHO one of the best startup attorneys in Finland)

Sweden

The WISE convertible, inspired by YC’s SAFE note

Germany

Convertible note, created by TheFamily

UK

Convertible note, created by Seedcamp

US

Convertible note, also created by Seedcamp

SAFE, created by YCombinator

More articles on the topic

Here are some related articles to check out: